How Do Fixed Indexed Annuities Work?

If you’ve been researching retirement planning, you’ve probably heard about fixed indexed annuities, sometimes called FIAs.

Many people like the idea of protecting their retirement savings while still having the opportunity to earn interest linked to the stock market.

But one question comes up more than any other:

How do fixed indexed annuities actually work?

The good news is that the basic concept is easier to understand than most people think.

Let’s walk through it step by step.

Step 1: You Purchase an Annuity

A fixed indexed annuity is a contract between you and a life insurance company.

You can usually fund it in one of two ways:

- A single lump-sum payment

- A transfer or rollover from another qualified retirement account, if allowed under applicable rules

Once your money is in the annuity, the insurance company begins managing the contract according to its terms.

Unlike buying stocks or mutual funds, you are purchasing an insurance product designed for long-term retirement planning.

Step 2: Your Money Is Not Invested Directly in the Stock Market

This is one of the biggest misunderstandings about fixed indexed annuities.

Even though your annuity may use an index such as the S&P 500®, your money is not directly invested in the stock market.

Instead, the insurance company measures how a market index performs over a specific period.

That performance may be used to determine how much interest is credited to your contract, based on the rules in your annuity.

This is why fixed indexed annuities are often described as offering growth potential without direct market investment.

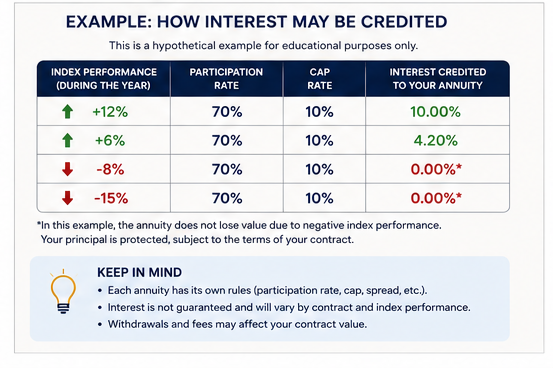

Step 3: Interest May Be Credited Based on Index Performance

Every annuity has a method for calculating interest.

If the index performs well, your annuity may receive interest according to the contract’s crediting method.

Insurance companies use different approaches, including:

- Participation rates

- Interest caps

- Spread rates

- Fixed-rate options

For example, suppose an index increases by 10% during the contract year.

Your annuity does not automatically receive 10%.

Instead, the amount credited depends on your contract’s specific provisions.

This is one reason it is important to compare products carefully before making a decision.

A simple overview of the five basic steps of how a fixed indexed annuity works.

Step 4: What Happens if the Market Goes Down?

This is where many retirees become interested in fixed indexed annuities.

If the market index has a negative return, many contracts include a floor that prevents negative index performance from reducing your protected principal.

For example:

Imagine you place $200,000 into a fixed indexed annuity.

During the next year:

- The market index drops by 18%.

With many fixed indexed annuities, your contract would generally not lose value because of that negative index performance.

This feature can help reduce the emotional stress some retirees feel during periods of market volatility.

Keep in mind that this protection applies to market performance under the contract terms. Surrender charges, rider fees, or withdrawals can affect your contract value.

A simplified example showing how positive index performance may result in credited interest while negative index performance may not reduce protected principal under the contract terms.

Step 5: Your Earnings Grow Tax Deferred

Another benefit many people appreciate is tax-deferred growth.

With most non-qualified fixed indexed annuities:

- You generally do not pay taxes each year on credited interest.

- Taxes are generally due when earnings are withdrawn.

Tax deferral allows earnings to remain in the contract and continue compounding until withdrawals begin.

Always consult a qualified tax professional regarding your personal tax situation.

Step 6: You Can Choose When to Receive Income

Many people purchase a fixed indexed annuity because they want dependable retirement income.

Depending on your contract, you may have several options.

These can include:

- Taking occasional withdrawals

- Receiving payments for a specific number of years

- Electing guaranteed lifetime income if available under the contract

Lifetime income is designed to help address one of the biggest retirement concerns—outliving your savings.

Understanding Important Terms

When comparing fixed indexed annuities, you’ll often see a few common terms.

Participation Rate

A participation rate determines how much of an index’s increase may be used when calculating interest.

Interest Cap

Some contracts place a maximum limit on the interest that can be credited during a measuring period.

Spread

A spread is a percentage deducted from the index gain before interest is credited.

Each insurance company sets these features according to its product design.

Why Do People Choose Fixed Indexed Annuities?

Every retiree has different goals.

Some people are comfortable taking significant investment risk.

Others want greater stability.

A fixed indexed annuity may appeal to people who want:

- Protection from negative market performance under contract terms

- Growth potential linked to a market index

- Tax-deferred growth

- Predictable retirement planning

- Optional lifetime income features

Many retirees use a fixed indexed annuity for only a portion of their retirement savings while keeping other assets invested elsewhere.

Frequently Asked Questions

Is my money invested in stocks?

No. Your money is not directly invested in the stock market. Interest is calculated using a market index according to the contract rules.

Can I lose money if the market crashes?

Many fixed indexed annuities are designed so that negative market performance does not reduce protected principal. However, surrender charges, withdrawals, or other contract provisions may affect value.

Do all fixed indexed annuities work the same way?

No. Different insurance companies use different crediting methods, participation rates, caps, spreads, riders, and surrender periods.

Are fixed indexed annuities only for retirees?

They are most commonly used by people who are close to retirement or already retired, although suitability depends on each person’s financial goals and circumstances.

How long should I plan to keep one?

Most fixed indexed annuities are designed as long-term financial products and include surrender-charge periods that vary by contract.

Final Thoughts

A fixed indexed annuity combines several features that many retirees find attractive.

It offers the opportunity to earn interest linked to a market index without directly investing in the stock market. Many contracts also provide principal protection from negative index performance and the option to create guaranteed lifetime income.

Like any financial product, a fixed indexed annuity should be evaluated carefully. Understanding how interest is credited, how withdrawals work, and what guarantees are included can help you decide whether it belongs in your retirement strategy.

Learning how these products work is the first step toward making informed retirement decisions.

Retirement planning doesn’t have to be confusing.

If you’d like to learn whether a fixed indexed annuity may fit your retirement goals, speak with a licensed insurance professional who can explain your options and help you compare available solutions based on your individual needs.

{kind=link}

{kind=link}

Leave A Comment

You must be logged in to post a comment.