Can You Lose Money in a Fixed Indexed Annuity?

One of the first questions people ask about fixed indexed annuities is:

“Can I lose money?”

It’s an important question, especially if you’ve spent years saving for retirement.

Many retirees want the opportunity to grow their savings, but they also worry about what could happen if the stock market drops.

The answer is a little more detailed than a simple “yes” or “no.”

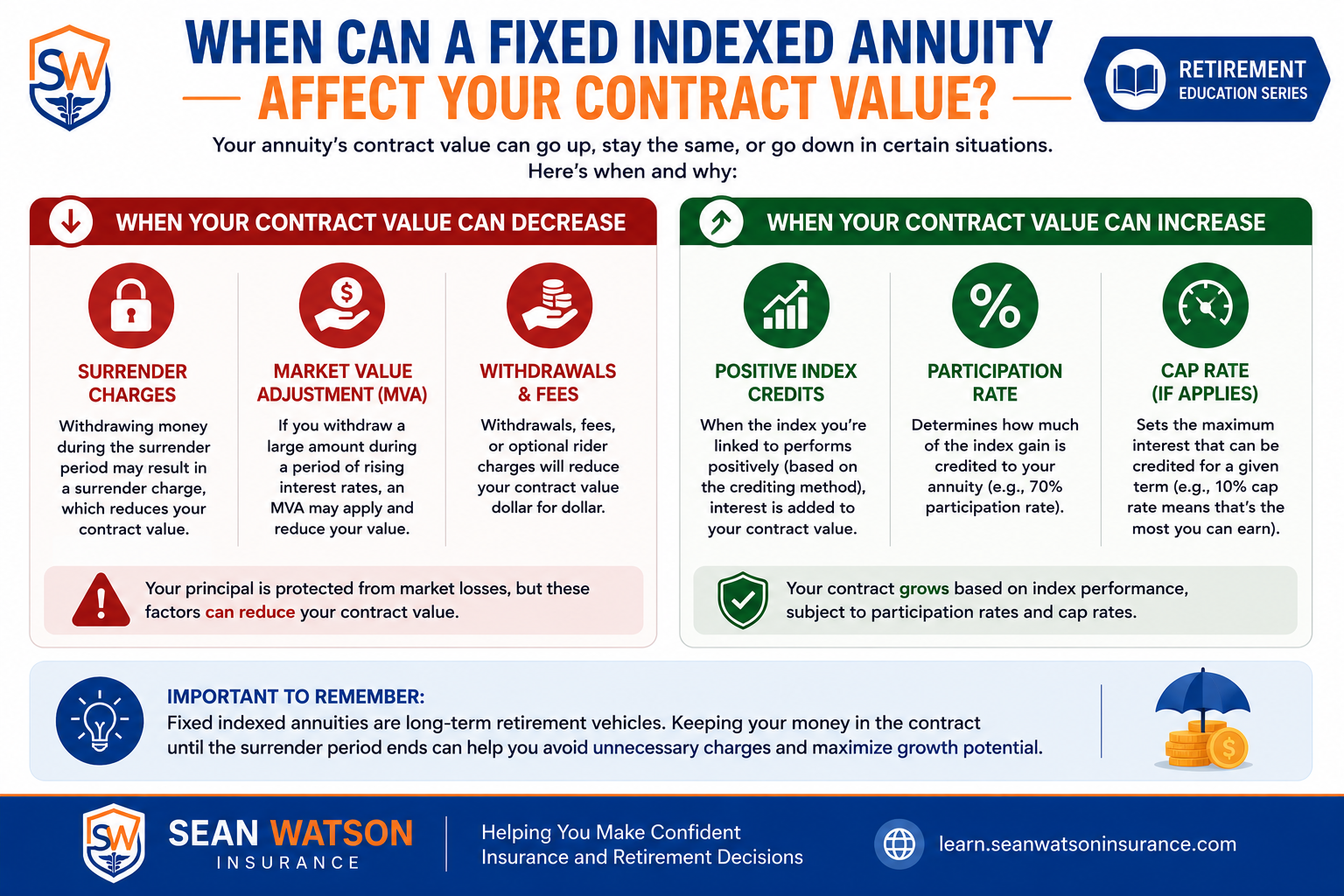

The good news is that many fixed indexed annuities are designed so that negative market performance does not reduce your protected principal. However, there are other situations that every buyer should understand before making a decision.

Let’s take a closer look.

Understanding Principal Protection

One of the biggest reasons people consider a fixed indexed annuity is something called principal protection.

Your principal is the money you put into the annuity.

With many fixed indexed annuities, if the market index declines, your protected principal generally does not decrease because of that negative market performance.

Imagine this example.

You purchase a fixed indexed annuity with $250,000.

During the next year, the market index falls by 22%.

If your contract includes protection against negative index performance, your principal would generally not lose value because of that market decline.

That feature is very different from owning investments that move up and down with the market every day.

It is one reason many retirees use a fixed indexed annuity to help protect a portion of their retirement savings.

Your Money Is Not Invested Directly in the Stock Market

This is another point that often causes confusion.

Although many fixed indexed annuities use an index such as the S&P 500® to calculate interest, your money is not directly invested in stocks.

Instead, the insurance company measures how the index performs over a specific period.

If the index increases, your contract may receive interest according to the rules in your annuity.

If the index has a negative return, many contracts include a floor that prevents losses caused by negative index performance.

Because your money is not directly invested in the market, your contract generally does not experience the same day-to-day ups and downs that investors see in stock portfolios.

Does That Mean There Is Absolutely No Risk?

Not exactly.

While many fixed indexed annuities protect against losses caused by negative market performance, that does not mean there are no risks or trade-offs.

Like every financial product, fixed indexed annuities have rules that you should understand before purchasing one.

Knowing these rules helps you decide whether the product fits your retirement goals.

Situation #1: Taking Out Too Much Money Too Soon

Most fixed indexed annuities are designed to be long-term retirement products.

Because of that, many contracts include a surrender period.

During this time, you may be allowed to withdraw a limited amount each year without a surrender charge.

However, taking out more than the contract allows could result in a surrender charge.

Example

Suppose your contract allows a 10% penalty-free withdrawal each year.

If you withdraw 25% of your account value during the surrender period, the amount above the penalty-free limit may be subject to surrender charges.

These charges usually decrease over time until they eventually expire.

This is one reason financial professionals often recommend using money that you do not expect to need for immediate expenses.

While many fixed indexed annuities protect against negative market performance, withdrawals above the contract’s penalty-free limit during the surrender period may result in surrender charges.

Situation #2: Optional Riders May Have Additional Costs

Many fixed indexed annuities offer optional features called riders.

A rider can provide additional benefits.

For example, some riders may offer:

- Guaranteed lifetime income

- Enhanced death benefits

- Long-term care or chronic illness benefits (if available)

Some riders are included at no additional cost.

Others have an annual fee.

That does not necessarily mean the rider is a poor value.

In many cases, retirees gladly pay for benefits that provide additional financial security.

The important thing is understanding exactly what the rider provides and how any fee may affect your contract over time.

Always review the rider disclosure carefully before making a decision.

Situation #3: The Insurance Company’s Financial Strength Matters

When you purchase a fixed indexed annuity, you are entering into a contract with an insurance company.

The guarantees in your annuity are backed by the claims-paying ability of the issuing insurance company.

That is why many financial professionals encourage reviewing an insurer’s financial strength ratings from independent rating organizations before purchasing an annuity.

Companies with strong financial ratings have demonstrated financial stability over time, although ratings can change and are not guarantees of future performance.

Working with a knowledgeable insurance professional can help you compare products from financially strong insurers.

What Happens During a Market Crash?

Let’s look at a simple example.

Assume two retirees each have $300,000.

Retiree A invests directly in the stock market.

Retiree B places a portion of retirement savings into a fixed indexed annuity with protection against negative index performance under the contract terms.

If the market falls by 30%:

Retiree A’s investment account could decline in value based on market performance.

Retiree B’s fixed indexed annuity generally would not lose principal because of that negative index performance, assuming no withdrawals or other contract adjustments apply.

This example illustrates why many retirees view fixed indexed annuities as one tool for helping manage market volatility.

It does not mean they are appropriate for everyone or that they replace every type of investment.

What If Your Annuity Earns 0% Interest?

Another question many people ask is:

“What happens if the market doesn’t go up?”

Because fixed indexed annuities earn interest based on the performance of a market index, there may be years when your contract is credited with 0% interest.

That can happen if:

- The market index has a negative return.

- The market index finishes flat.

- The contract’s crediting method does not result in interest for that measuring period.

For some retirees, earning 0% during a difficult market year is preferable to experiencing a large market loss.

Imagine this example.

Retiree A has money invested directly in the stock market.

Retiree B owns a fixed indexed annuity.

The market falls 18%.

Retiree A’s account value declines along with the market.

Retiree B earns 0% interest that year but does not lose principal because of the market decline, assuming the contract provides protection against negative index performance and no withdrawals or other contract adjustments apply.

Over time, avoiding significant losses may help some retirees preserve more of their retirement savings.

A Fixed Indexed Annuity Is Designed for Long-Term Retirement Planning

A fixed indexed annuity should not be viewed as a short-term investment.

Instead, it is generally designed for people who want to:

- Protect part of their retirement savings.

- Reduce exposure to market downturns.

- Create dependable retirement income.

- Grow money on a tax-deferred basis.

- Leave a financial legacy to loved ones, depending on the contract’s death benefit provisions.

Many retirees choose to place only a portion of their retirement assets into a fixed indexed annuity while keeping the rest in other investments.

That approach can help balance growth opportunities with principal protection.

Common Myths About Losing Money in a Fixed Indexed Annuity

Let’s clear up a few common misunderstandings.

Myth #1: “I Can Lose Everything if the Stock Market Crashes.”

Fact:

Many fixed indexed annuities are designed so that negative market performance does not reduce protected principal under the contract terms.

Your contract value generally does not move up and down with the stock market the way a brokerage account does.

Myth #2: “My Money Is Invested in Stocks.”

Fact:

Your money is not directly invested in the stock market.

The market index is used as a benchmark for calculating interest according to the contract’s rules.

Myth #3: “Every Fixed Indexed Annuity Is the Same.”

Fact:

No two contracts are exactly alike.

Insurance companies may offer different:

- Participation rates

- Interest caps

- Spread rates

- Surrender periods

- Income riders

- Death benefit options

Comparing products carefully is an important part of choosing the right annuity.

Myth #4: “I Should Put All My Retirement Savings Into an Annuity.”

Fact:

A fixed indexed annuity is often used as one part of a retirement plan.

Many retirees choose to diversify by keeping some assets in other investments while using an annuity to help create stability and income.

A simplified comparison showing how many fixed indexed annuities are designed to protect principal from negative index performance, while investments held directly in the market generally fluctuate with market conditions.

Questions to Ask Before Purchasing a Fixed Indexed Annuity

Before purchasing any retirement product, ask these important questions:

- How long is the surrender period?

- How is interest calculated?

- Does this annuity include an income rider?

- Are there any rider fees?

- What withdrawal options are available?

- What happens if I pass away?

- What are the financial strength ratings of the insurance company?

- Does this product fit my retirement income goals?

The answers can help you compare contracts and choose a solution that matches your needs.

Frequently Asked Questions

Can I lose money because the market goes down?

Many fixed indexed annuities are designed so that negative market performance does not reduce protected principal under the contract terms. However, surrender charges, withdrawals, rider fees, or other contract provisions may affect your contract value.

Can I lose money if I withdraw funds early?

Possibly.

Most contracts include a surrender period. Withdrawals above the contract’s penalty-free limit during that period may result in surrender charges.

What happens if my annuity earns 0%?

Many retirees view a 0% credited interest year differently than a negative return because their protected principal is generally not reduced due to negative market performance, assuming the contract provides that protection.

Is a fixed indexed annuity guaranteed?

Certain guarantees are provided by the contract and are backed by the claims-paying ability of the issuing insurance company.

Is a fixed indexed annuity right for everyone?

No.

Every retirement plan is different.

A fixed indexed annuity may be appropriate for some people, while others may benefit from different financial strategies depending on their goals, income needs, liquidity requirements, and risk tolerance.

Final Thoughts

Can you lose money in a fixed indexed annuity?

The answer depends on what you mean by “lose money.”

Many fixed indexed annuities are designed so that negative market performance does not reduce protected principal under the contract terms.

However, surrender charges, optional rider fees, and early withdrawals can affect your contract value.

Understanding how these products work—and what they are designed to do—can help you make more informed retirement decisions.

A fixed indexed annuity is not designed to eliminate every risk.

Instead, it is intended to help many retirees balance growth potential, principal protection, and dependable retirement income as part of a well-rounded financial strategy.

Continue Learning

Want to learn more about fixed indexed annuities?

Continue reading these guides:

- What Is a Fixed Indexed Annuity?

- How Do Fixed Indexed Annuities Work?

- Fixed Indexed Annuity vs. CD: Which Is Better for Retirement?

- Fixed Indexed Annuity Pros and Cons

- What Is an Income Rider?

Every retirement journey is different.

If you’re wondering whether a fixed indexed annuity may fit your retirement goals, speaking with a licensed insurance professional can help you understand your options, compare available products, and make an informed decision based on your unique financial situation.

No one solution fits everyone—but having the right information is an excellent place to start.

{kind=link}

{kind=link}

Leave A Comment

You must be logged in to post a comment.