If you are someone you know has been diagnosed with End-Stage Renal Disease [also known as Chronic Kidney Disease Stage 5] many questions may come to mind. Chief among them how will you be able to afford treatment for yourself or your loved one. Today we’re going to discuss health insurance options for End-Stage Renal Disease sufferers.

Healthcare is expensive, and prices continue to rise with no sign of slowing down. Based on the most recent data, End-Stage Renal Disease cost Medicare nearly 33 billion dollars per year, or 7.2% of all Medicare spending, statistics that continue to rise with each passing year. Dialysis treatments cost an average of $89,000 per year – up from $72,000 per year only four years ago.[1] On average a kidney transplant cost upwards of $300,000 with an estimated out-of-pocket cost of $32,000 for the surgery. Individuals can expect an additional cost of $25,000 per year afterward for post-surgery care in the form of immunosuppressants.[2]

Luckily, there are multiple health insurance options to consider when planning for care. In this article, we review some basic facts about End-Stage Renal Disease and the different health insurance options for treatment. We also discuss secondary insurance options, sometimes known as second healthcare payers.

What is End Stage Renal Disease?

End Stage Renal Disease (ESRD) occurs when the kidneys permanently fail to work. Your kidneys are two fist-sized bean-shaped organs that are responsible for filtering the extra waste and water out of your blood and produce urine. ESRD occurs when your kidneys can no longer perform this function as needed for day-to-day life. ESRD is generally diagnosed through a combination of blood tests, urine tests, ultrasounds, kidney biopsy’s, and CT Scans. The most common causes of ESRD are diabetes, high blood pressure, heart disease, and a family history of the condition. ESRD can be the result of either acute or chronic kidney disease. Acute Kidney Injury (AKI) is the sudden or temporary loss of kidney function. Chronic Kidney Disease (CKD) is the reduction of kidney function over a period of time. Chronic Kidney Disease is by far the most common cause of ESRD. Your physician can provide you specific information regarding your diagnosis and available treatment options.

You can work to prevent ESRD by managing those conditions, such as diabetes and high blood pressure that causes the disease. Other steps you can take to prevent ESRD and Kidney Disease include making health food choices, taking part in regular physical activity, aiming for a healthy weight, stop smoking, ensuring you are getting enough sleep, limiting your alcohol intake, taking part in stress-reducing activities, and managing diabetes, high-blood pressure, and heart disease. As always, you want to discuss your options with your healthcare provider to determine what is best for you.[3] Your healthcare provider can assist in locating services and activities to help reduce your risk of ESRD.

Overall, ESRD affects nearly 650,000 people per year in the United States, a figure that is growing by 5% each year. Compared to whites, African-Americans are 3.5 times more likely to develop ESRD and Hispanics are 1.5 times more likely to develop ESRD. In the United States, more men are diagnosed each year with ESRD and individuals between the age of 45 to 64 represent 44% of cases.[4]

Treating End-Stage Renal Disease

Kidney transplantation remains the best method of treating ESRD. Yet, while the need for donor’s kidneys is rising at 8% per year, the availability of donor’s kidneys is not keeping up. In the previous years, while nearly 100,000 kidneys were needed, less than 20,000 were available each year. This has resulted in waiting periods on the transplant list of 3 to 5 years, or longer. Once a successful surgery has occurred individuals must still be prepared to remain on immunosuppressants for the rest of their lives. These immunosuppressants assist the body in accepting the new organ and not rejecting it.

Outside of receiving a kidney transplant, the only alternative remains dialysis. Dialysis treatment consists of filtering the patient’s blood through an external system before pumping it back into the body. In this regard, the dialysis treatment serves to replace the lost function of the kidneys in filtering the bodies waste.[5]

Individuals receiving dialysis can expect to be required to receive treatment at least three times a week with each dialysis session lasting between 3 to 5 hours. Most individuals are required to travel to certified medical facilities to receive treatment, increasing both the time required for treatment and the cost associated with treatment due to travel.[6] In-home dialysis treatment is available in some areas, however the cost

You need to work with your physician and medical team in developing your care plan and identifying all treatment options that may be available to you.

Paying for Treatment End Stage Renal Disease

When you become ill, the last thing you want to think about is the cost of care. However, healthcare cost is not something to take lightly. Expenses can rapidly pile up. It can be confusing with the constant flood of different bills from different providers of your medical team. You want to quickly identify your available options and resources and work towards gaining an understanding of what each does and does not cover. While identifying potential cost and payment options may not be the first thing you consider with a new diagnosis, taking this vital step early on provides ease-of-mind as you move throughout treatment. Doing so will also assist in identifying opportunities to supplement your health insurance with other options.

Understanding the basics of ESRD health insurance payment is something you or your loved one wants to do.

There are some important health insurance terms you should be familiar with during this process:

Primary Insurance: The primary health insurance is the insurance that pays on the bill first. Generally, it will cover a specific dollar amount or percentage of your medical bill.

Secondary Insurance: The secondary health insurance is the insurance that pays the bill second. For most individuals with ESRD, this secondary health insurance covers the remaining cost that the primary insurance did not.

Benefit Period: Used by Medicare Part A and B to measure your use of hospital and skilled nursing facility (SNF) services. A benefit period begins the day you are admitted to a facility. The benefit period ends when you have not received any inpatient care for 60 days in a row. If you enter an inpatient care facility after one benefit period ends, you enter a new benefit period. There is no limit to the number of benefit periods.

Deductible: The amount you must pay for medical services before your health insurance begins to pay.

Coinsurance: Coinsurance is the amount you may be required to pay for any medical services after you pay the deductible. Generally, coinsurance is a percentage (for example, 20%)

Copayment: Co-payment is different from coinsurance. A copayment is an amount you may be required to pay for your cost of the medical service. Unlike coinsurance, a copayment is generally a dollar amount (for example, $35).

Coordination of Benefits Rule: The process of identifying what health insurance is the primary and which is the secondary. The primary will pay up to the limits of coverage whereas the secondary payer will only pay if there is additional cost the primary insurance did not cover. The secondary payer may not pay all the additional cost. You can find out more information on which insurance pays first in your specific situation by visiting Medicare.gov.

Out-of-Pocket-Cost: Out-of-pocket cost is those cost you are required to pay on your own as they are not covered by any insurance option.

Premium: The payment to an insurance company, or Medicare, for your health insurance coverage.

For most individuals, Medicare serves as the primary insurance with a Medicare Supplement Insurance (Medigap) policy serving as your secondary insurance option.

If you have an Employer Group Health Plan, generally provided through your place of employment, your Employer Group Health Plan will serve as your primary insurance for the first 30 months after starting dialysis or following your kidney transplant. Following this 30-month period, Medicare becomes your primary insurance and your Employer Group Health Plan your secondary insurance. It is important to note even in these situations the Employer Group Health Plan may not cover all the cost associated with treatment. You will want to inform your Employer Group Health Plan that you have activated your Medicare insurance. Doing so assist in ensuring everything is billed appropriately.

Below we discuss the Medicare and secondary insurance options available to individuals with ESRD.

Medicare

When most people here ‘Medicare’ they immediately think it is only for individuals age 65 and over. In fact, Medicare is government health insurance available to:

- People age 65 and older

- People under age 65 with specific disabilities

- People of any age with End-Stage Renal Disease

As you can see, there is a special carve-out that makes Medicare health insurance available to those who are diagnosed with ESRD. You are eligible to get Medicare, regardless of age, if your kidneys no longer function, you need regular dialysis or you have had a kidney transplant, and if one of the following applies to you:

- You have worked the required amount of time under Social Security, the Railroad Retirement Board, or as a government employee.

- You are already receiving or are eligible for Social Security or Railroad Retirement Board

- You are the spouse or dependent child of a person who meets the above requirements.

If you are eligible for Medicare due to ESRD and you meet the above requirements, you will need to contact your local Social Security Office. You can also enroll and locate your local Social Security Office by calling 1-800-772-1213 (TTY users can call 1-800-325-0778).

When you enroll in Medicare as part of an ESRD diagnosis, you will most likely be eligible for what is known as ‘Original Medicare.’ Medicare today is divided into four parts:

- Medicare Part A: Hospital Insurance

- Medicare Part B: Medical Insurance

- Medicare Part C: Medicare Advantage

- Medicare Part D: Prescription Drug Coverage.

Medicare Parts A and B are known as original Medicare as they were part of the original Medicare program in 1966. While Medicare Part C (Medicare Advantage) has similar coverage to Medicare Parts A and B, ESRD individuals who are not otherwise eligible for Medicare will not be able to select Part C.

When signing up, it is essential to understand what coverage you have access to.

Medicare Part A (also known as Hospital Insurance) helps to cover:

- Inpatient hospital care

- Inpatient care in a skilled nursing facility

- Hospice care

- Home health care

Medicare Part B (also known as Medical Insurance) helps to cover:

- Doctor services and other healthcare provider services

- Outpatient care

- Home health care

- Select preventive services

When you enroll in Medicare under the ESRD provision, you will be able to access any doctor or medical supplier that is enrolled in and accepts Medicare payment and is accepting new patients at that time. You will also be able to access any participating hospital or other facilities, such as dialysis clinic, that accepts Medicare and is taking in new patients.

For most individuals, there is no monthly premium for Medicare Part A. This is because you, or your spouse, paid Medicare taxes while working. Most people pay a monthly premium for Part B. The premium rate for Part B changes yearly and may be higher based on your income. For 2017 the average premium was $134 per month.

Keep in mind; you need Part B to receive your full benefits, including dialysis treatment.

Multiple medical events can provide you access to the Medicare coverage for ESRD. When developing your care plan, you want to take into consideration the different triggering events and plan out what is best for you.

According to the Centers for Medicare and Medicaid Services, when individuals enroll in Medicare due to ESRD, the Medicare coverage generally starts:

When the beneficiary first enrolls in Medicare based on ESRD, Medicare coverage usually starts:

- During the fourth month of dialysis treatment when the individual participates in dialysis treatments within a certified- dialysis facility.

- Medicare coverage can start as early as the first month of dialysis if:

-

- The individual is eligible and is taking part in a home dialysis training program in a Medicare-approved facility with the goal of learning how to carry out treatment at home;

- The individual begins home dialysis treatment training before the third month of dialysis: &

- The individual expects to finish home dialysis training and be able to carry out self-dialysis treatments at home.

- Medicare coverage can start the month the individual is admitted to a Medicare-approved hospital for a kidney transplant or the health services that are needed before the transplant, so long as the transplant takes place within two months.

- Medicare coverage can start two months before transplant if the transplant is delayed more than two months once someone has been admitted to the hospital for transplant or transplant-related services.

- This triggering event includes both if the individual starts pre-surgical care before the transplant and if the transplant is delayed.

Ideally, if an individual has accessed Medicare only because of ESRD, the Medicare coverage ends. Medicare coverage for an individual with ESRD only (someone who does not meet the other criteria for Medicare) will end, also known as terminate, when one of the following conditions are met:

- 12 months after the month the individual stops receiving dialysis treatments, OR

- 36 months after the month the individual has received a kidney transplant.

An individual whose Medicare coverage has ended may have the coverage started again. The coverage may be resumed if:

- Dialysis treatment begins again, or you get a kidney transplant within 12 months after the month you stopped getting dialysis.

- The individual starts dialysis or gets another kidney transplant 36-months after the month after the month of the initial transplant.

For someone with an Employer Group Health Plan, this requires a separate 30-month coordination period.[7] The Centers for Medicare and Medicaid provide the following examples to help explain.

“If an individual receives a kidney transplant that continues to work for 36 months, the Medicare coverage will end (unless you are eligible for Medicare also due to age or disability). If after 36 months you enroll in Medicare again because you start dialysis or receive another transplant, your Medicare coverage starts right away. There is no-3 month waiting period. However, there is a new 30-month coordination period with an Employer Group Health Plan.”

If you are someone who has an Employer Group Health Plan you may be wondering if you must use Medicare to pay for treatment. You do not. However, you want to think about your decision carefully. You want to review all your benefits and plan details. Medicare Part A and B can assist in defraying some of the deductible, copayment, or coinsurance cost. You should also think about future coverage needs, including for immunosuppressive drugs if you receive a kidney transplant.

You can delay your enrollment until the end of the 30-month coordination period.

So, What Does Medicare Cover?

You may be asking yourself what exactly is covered under Medicare and your insurance. For any Employee Group Health Plan, you want to consult with the appropriate health plan representative. We are going to focus on the services provided by Medicare (Part A and B).

For dialysis, Medicare Part A covers your inpatient dialysis treatments. When considering a kidney transplant, Part A covers your inpatient services, kidney registry fee, laboratory or other test needed to evaluate your or a potential donors conditions, the full cost of care for a kidney donor, and blood for surgery.

For dialysis, Medicare Part B will cover outpatient dialysis treatments, select outpatient doctors’ services, home dialysis training, home dialysis equipment and supplies, certain home support services, most prescriptions needed for dialysis, and other required services as part of dialysis. When considering a kidney transplant, Part B will cover your doctors’ services for the surgery and your hospital stay, and a limited amount of immunosuppressive drugs. (You should review your options, including Medicare Part D, for covering your prescription drug cost). In select situations, Medicare Part B also covers ambulatory transfer to a dialysis clinic.

Medicare (Part A and B) do not cover: paid dialysis aides to help you with home dialysis, any lost pay due to home dialysis training, a place to stay during treatment, blood or red blood cells for home dialysis (unless part of a doctor’s service).

Once again, remember that you must sign-up for Part B and pay the monthly premium.

For dialysis, Medicare generally pays 80% of the amount, once you have paid the Part B yearly deductible ($183 in 2018). The patient is then responsible for the remaining 20% coinsurance.

Consider this example: One dialysis treatment can cost $480. Medicare would pay 80% of this cost (once the deductible is met) or $384. The coinsurance amount the patient would be responsible for would be $96.

Medicare pays 80% of doctor’s services, once the deductible is met. Medicare also covers 100% of Medicare-approved laboratory test and select blood services.

As an individual with ESRD, it is also necessary to understand the hospital services and skilled nursing facility (SNF) benefits under Medicare.

For hospital services under Medicare Part A and B you will pay:

- $1,316 deductible per benefit period

- Days 1–60: $0 coinsurance for each benefit period

- Days 61–90: $329 coinsurance per day of each benefit period

- Days 91 and beyond: $658 coinsurance per each “lifetime reserve day” after day 90 for each benefit period (up to 60 days over your lifetime)

- Beyond lifetime reserve days: all costs

Consider this example: An individual with ESRD is placed in the hospital for 30 days. What is their cost? After paying the $1,316 deductible, there is $0 coinsurance required for hospital services.

Consider this example: An individual with ESRD is in the hospital for 62 days following the end of one benefit period. What is the individual cost? After paying the $1,316 deductible, there is $0 coinsurance required for hospital services (keep in mind, some services received in the hospital may not be considered hospital services and billed differently) for days 1-60. For days 61 and 62 there is a $329 coinsurance per day. The total for this stay would be at least $1,974.

For Medicare-approved Skilled-Nursing Facilities you will pay:

- Days 1-20: $0 for each benefit period

- Days 21-100: $164.50 coinsurance per day for each benefit period

- Days 101 and beyond: all cost.

Consider this example: Following a successful kidney transplantation an individual is placed in a Skilled-Nursing Facility for 22 days. What is their cost? For days 1-20 there is a $0 coinsurance. For days 21 and 22 there is $164.50 coinsurance cost per day per benefit period. The total for this stay would be around $329.

These examples are provided only for illustrative purposes. Actual services rendered and secondary insurance can affect the cost. Keep in mind, services provided during a stay in a hospital or skilled nursing facility may be billed under specific codes.

Secondary Insurance Options

While Medicare provides coverage for ESRD patients, it should be clear Medicare does not cover 100% of the cost.

Consider the previous example of receiving dialysis treatment. One dialysis treatment can cost $480. Medicare pays 80% of this cost (once the deductible is met) or $384. The patient is responsible for the $96 coinsurance amount. Assuming three treatments per week, this would be $288 per week or $14,976 per year for dialysis treatment alone.

Secondary insurance can assist in alleviating the burden of these costs. Outside of Employer Group Health Plans one option that exists are Medicare Supplement Insurance policies, also known as Medigap.

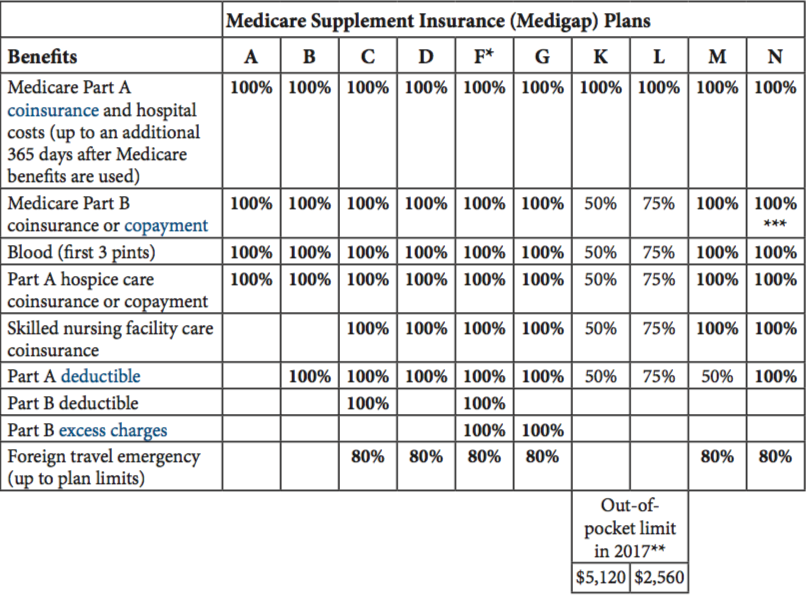

Medigap policies are health insurance policies sold by private insurance companies to assist in filling the ‘gaps’ in Medicare Part A and B coverage, such as deductibles and coinsurance. These policies pay some of the cost the Medicare Part A and B do not cover. A Medigap policy is different from a Medicare Advantage Plan (Medicare Part C). Medigap supplements Medicare Parts A and B, it does not replace it.

Medigap policies are identified by letters by specific letters (A-N, with E, H, I, and J no longer being sold) Medigap policies are clearly labeled as “Medicare Supplemental Insurance” and offer standard benefits. Premium price differences represent different services and benefits provided by the insurance company beyond the standard benefit.

The below chart summarizes what the each of the standardized Medigap policies cover.

Medigap Plans offered by Sean Watson

Insurance companies are not required to offer every Medigap policy. They must offer Plan A if they offer any Medigap policies. If they offer plans in addition to Plan A, they are also required to offer Plan C or Plan F. You can buy Medigap policies during a 6-month period known as open enrollment. The six-month period occurs once you have signed up for Medicare Part B. After this open-enrollment period (six-months) you may have the option to sign-up, but the cost might be higher.

Not all states have Medigap policies available to those under the age of 65. If you are diagnosed with ESRD before age 65, you may be unable to locate a Medigap policy in your state. Some states require that at least one Medigap policy be made available to those under 65. A listing of those states is provided below.

These States Offer Medicare Supplement Plans For Individuals Under Age 65 |

||

| Colorado | Louisiana | North Carolina |

| Connecticut | Maine | Oklahoma |

| Delaware | Maryland | Oregon |

| Florida | Massachusetts | Pennsylvania |

| Georgia | Michigan | South Dakota |

| Hawaii | Minnesota | Tennessee |

| Idaho | Mississippi | Texas |

| Illinois | Missouri | Wisconsin |

| Kansas | Montana | Wisconsin |

| Kentucky | New Hampshire | |

| New Jersey | New York | |

Let’s consider some specific state Medigap options that individuals with ESRD may want to consider.

State Specific Secondary Option

Note: That your premium is dependent on your health condition, are of residence, gender, smoking status, and other factors. Averages provided are based on a fictional male with an unknown health status living in the zip code of the state capital. You should contact your selected insurance provider to receive an accurate quote.

Colorado

In Colorado, all Medigap plans (A, B, C, D, F, G, K, L, M, N) sold by a company must be offered to all individuals if they meet the eligibility requirements for Medicaid. The cost for individuals below age sixty-five may be higher.

A total of 34 insurance companies offer Medigap Insurance Policy A. Fourteen (14) offer Medigap Policy B, 17 offer Medigap Policy C, 9 offer Medigap Policy D, 34 offer Medigap Policy F, 19 offer Medigap Policy G, 6 offer Medigap Policy K, 6 offer Medigap Policy L, 3 offer Medigap Policy M, and 26 offer Medigap Policy N.

The monthly average premium range between $32 and $329, depending on the plan.

Florida

In Florida, all Medigap plans (A, B, C, D, F, G, K, L, M, N) sold by a company must be offered to all individuals if they meet the eligibility requirements for Medicaid. The cost for individuals below age sixty-five may be higher.

A total of 25 insurance companies offer Medigap Insurance Policy A. Thirteen (13) offer Medigap Policy B, 13 offer Medigap Policy C, 8 offer Medigap Policy D, 25 offer Medigap Policy F, 15 offer Medigap Policy G, 4 offer Medigap Policy K, 6 offer Medigap Policy L, 3 offer Medigap Policy M, and 18 offer Medigap Policy N.

The monthly average premium range between $76 and $505, depending on the plan.

Kansas

In Kansas, all Medigap plans (A, B, C, D, F, G, K, L, M, N) sold by a company must be offered to all individuals if they meet the eligibility requirements for Medicaid. The cost for individuals below age sixty-five may be higher.

A total of 49 insurance companies offer Medigap Insurance Policy A. Seventeen (17) offer Medigap Policy B, 21 offer Medigap Policy C, 10 offer Medigap Policy D, 49 offer Medigap Policy F, 31 offer Medigap Policy G, 7 offer Medigap Policy K, 7 offer Medigap Policy L, 8 offer Medigap Policy M, and 39 offer Medigap Policy N.

The monthly average premium range between $30 and $270, depending on the plan.

Maryland

Maryland requires only plans A and C to be offered to individuals under the age of 65. An insurance company may offer other plans to individuals under 65 if they meet the eligibility requirements for Medicaid. The cost for individuals below age sixty-five may be higher.

In Maryland, Medigap Policies A, B, C, F, K, L, and N are offered to individuals under the age of 65.

A total of 28 insurance companies offer Medigap Policy A. Two (2) offer Medigap Policy B, 6 offer Medigap Policy C, 28 offer Medigap Policy F, 1 offers Medigap Policy K, L, and N.

The monthly average premium range between $98 and $344, depending on the plan.

Missouri

In Missouri, all Medigap plans (A, B, C, D, F, G, K, L, M, N) sold by a company must be offered to all individuals if they meet the eligibility requirements for Medicaid. The cost for individuals below age sixty-five may be higher.

A total of 47 insurance companies offer Medigap Insurance Policy A. Eighteen (18) offer Medigap Policy B, 18 offer Medigap Policy C, 14 offer Medigap Policy D, 47 offer Medigap Policy F, 31 offer Medigap Policy G, 7 offer Medigap Policy K, 32 offer Medigap Policy L, 6 offer Medigap Policy M, and 37 offer Medigap Policy N.

The monthly average premium range between $30 and $397, depending on the plan.

Oregon

In Oregon, all Medigap plans (A, B, C, D, F, G, K, L, M, N) sold by a company must be offered to individuals below the age of 65 if they meet the Medicaid requirements for ESRD or disability. The cost for individuals below age sixty-five may be higher.

A total of 47 insurance companies offer Medigap Insurance Policy A. Seventeen (17) offer Medigap Policy B, 8 offer Medigap Policy C, 9 offer Medigap Policy D, 47 offer Medigap Policy F, 21 offer Medigap Policy G, 11 offer Medigap Policy K, 9offer Medigap Policy L, 5 offer Medigap Policy M, and 31 offer Medigap Policy N.

The monthly average premium range between $72 and $247, depending on the plan.

As you can see, the plans offered, the cost of the plans and the number of potential insurance companies vary among states. It is essential to research your specific situation to be informed of your opportunities. Your state health insurance commissioner or state health insurance assistance program (SHIP) can assist you in this process.

Conclusion

Although a diagnosis of ESRD may seem intimidating at first with the proper planning, it can be managed. You will want to familiarize yourself with your treatment plan, Medicare Benefits, and secondary insurance options, such as Medigap. You want to review the insurance options available to you and make informed decisions based on your financial situation. Doing so, with the appropriate professional assistance, can help ensure proper treatment and remove some of the financial burden associated with the disease. It also provides peace of mind to you and your loved ones as move forward with ESRD.

If you have additional questions or you would like to get some rates for Medigap plans in your area, please feel to schedule a free, no-obligation telephone appointment.

Additional Resources:

These additional resources may assist you as you move forward in your journey with ESRD:

Academy of Nutrition and Dietetics: https://www.eatright.org/

American Kidney Fund: http://www.kidneyfund.org/

American Association of Kidney Patients: https://aakp.org/

Dialysis Patient Citizens: http://www.dialysispatients.org/

National Kidney Foundation: https://www.kidney.org/

State Health Insurance Assistance Program: https://www.shiptacenter.org/

Disclaimer: Additional resources and citations are being provided as a convenience and for informational purposes only; they do not constitute an endorsement or approval. No claim or responsibility is made for the accuracy, legality or content of the external site or for that of subsequent links. Contact the external site for answers to questions regarding its content

[1] Data from: http://www.modernhealthcare.com/article/20141011/MAGAZINE/310119932

[2] U.S. Renal Data System, USRDS 2015 Annual Data Report: Atlas of End-Stage Renal Disease in the United States, National Institutes of Health, National Institute of Diabetes and Digestive and Kidney Diseases, Bethesda, MD, 2016. & the United States Renal Data System 2016 Chapter 11: Medicare Expenditures for Persons with ESRD

[3] To learn more, visit the National Institutes for Health page on Kidney Disease https://www.niddk.nih.gov/health-information/kidney-disease/chronic-kidney-disease-ckd/prevention

[4] See the National Kidney Foundation for more information: https://www.kidney.org/news/newsroom/factsheets/End-Stage-Renal-Disease-in-the-US

[5] For additional information see the Kidney Project at the University of California, San Francisco: https://pharm.ucsf.edu/kidney/need/statistics

[6] For additional information see: https://www.kidney.org/sites/default/files/docs/11-10-0307_dialysistransitionbk2_oct07_lr_bm.pdf

[7] To find out more about this process, visit the Centers for Medicare and Medicaid webpage: https://www.cms.gov/Medicare/Coordination-of-Benefits-and-Recovery/Coordination-of-Benefits-and-Recovery-Overview/End-Stage-Renal-Disease-ESRD/ESRD.html

[8] For additional information review the 2017 CMS Medigap Policy: https://www.medicare.gov/Pubs/pdf/02110-Medicare-Medigap.guide.pdf?

{kind=link}

Leave A Comment

You must be logged in to post a comment.